By Simon Johnson

Most of the current policy discussion concerning the

euro area is about austerity. Some people – particularly in German

government circles – are pushing for tighter fiscal policies in troubled

countries (i.e., higher taxes and lower government spending). Others –

including in the new French government — are more inclined to push for a more

expansive fiscal policy where possible and to resist fiscal contraction

elsewhere.

The recently concluded G20 summit is being interpreted

as shifting the balance away from the “austerity now” group, at least to some

extent. But both sides of this debate are missing the important

issue. As a result, the euro area continues its slide towards deeper

crisis and likely eventual disruptive break-up.

The underlying problem in the euro area is the exchange rate system itself – the fact that these European countries locked themselves into an initial exchange rate, i.e., the relative price of their currencies, and promised to never change that exchange rate. This amounted to a very big bet that their economies would converge in productivity – that the Greeks (and others in what we now call the “periphery”) would in effect become more like the Germans. Alternatively, if the economies did not converge, the implicit presumption was that people would move – i.e., Greek workers go to Germany and converge to German productivity levels by working in factories and offices there.

It’s hard to say which version of convergence was more

unrealistic.

In fact, the opposite happened. The gap between German and Greek (and other peripheral country) productivity increased, rather than decreasing, over the past decade. Germany, as a result, developed a large surplus on its current account – meaning that it exports more than it imports. The other countries, including Greece, Spain, Portugal and Ireland, had large current account deficits – they were buying more from the world than they were selling. These current account deficits were financed by capital inflows (including from Germany but also through and from other countries).

In theory, these capital inflows could have helped peripheral Europe invest, become more productive, and “catch up” with Germany. In practice, the capital inflows – in the form of borrowing – created the pathologies that now roil European markets.

In Greece, successive governments overspent – financed

by borrowing — as they attempted to stay popular and win elections. Some

of these same politicians will likely return to power following the elections

last weekend.

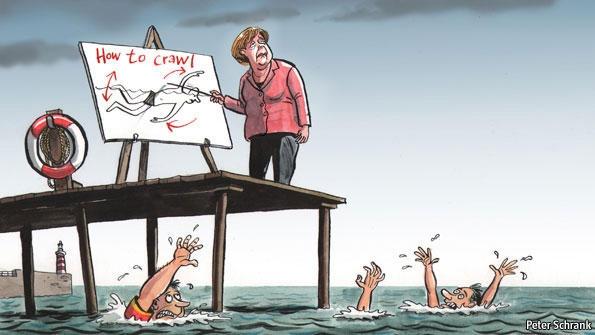

Greece has already adopted a considerable degree of

fiscal austerity. Now it needs to find its way to growth. Cutting

the budget further won’t do that. “Structural reform” – a favorite phrase

of the G20 crowd – takes a very long time to be effective, particularly to the

extent that it involves firing people in the short-run. Throwing more

“infrastructure” loans from Europe into the mix – for example, via the European

Investment Bank – is unlikely to make much difference. Additional loans

of this kind are likely to end up being wasted or stolen as more and more

well-connected people prepare for the moment when the euro is replaced by some

form of drachma.

In Spain and Ireland, capital inflows – through

borrowing by prominent banks – pumped up the housing market. The bursting

of that bubble has contracted their real economies and brought down all the

banks that gambled on loans to real estate developers and construction

companies. Their problems are not much to do with fiscal policy. As

conventionally measured, both Ireland and Spain had responsible fiscal policies

during the boom – but they were building up big contingent liabilities, in the

form of irresponsible banking practices.

When the banks blew up in Ireland, this created a

fiscal calamity for the government – mostly due to lost tax revenue. It

remains to be seen if Ireland can now find its way back to growth.

Spain still needs to recapitalize its banks – putting

more equity in to replace what has been wiped out by losses — and, most

important, must also find a renewed path to private sector growth.

Investors are rightly doubtful that the current policies are pointed in this

direction.

In Portugal and Italy, the problem is a long-standing

lack of growth. As financial markets become skeptical of European

sovereign debt, these countries need to show that they can begin grow steadily

– and bring down their debt relative to GDP (something that has not happened

for the past decade or so). Fiscal austerity will not help, but fiscal

expansion is also unlikely to do much – although presumably it could boost

headline numbers for a quarter or two. The private sector needs to grow,

preferably through exporting and through competing more effectively against

imports.

Peripheral Europe could, in principle, experience an

“internal devaluation”, in which nominal wages and prices fall, and they become

hypercompetitive relative to Germany and other trading partners. As a

matter of practical economic outcomes, it is hard to imagine anything less

likely.

Some politicians still hint they could produce the

rabbit of “full European integration” of the proverbial magic hat. What

does this imply about quasi-permanent transfers from Germany to Greece (and

others)? Who pays to clean up the banks? What happens to all the

government debt already outstanding? And does this mean that all Europe

would now adopt German-style fiscal policy?

These schemes are moving even beyond the far-fetched

notions that brought us the euro. “Europe only integrates in the face of

crisis” is the last slogan of the euro-enthusiasts. Perhaps, but crises

have a tendency to get out of control – particularly when they produce

political backlash.

Most likely, the European Central Bank will provide

some big additional “liquidity” loans to bring down government bond yields as

we head into the summer. We should worry about how long any such

feel-good policies last. Historically, August is a good month for a big

European crisis.

At these difficult times approach, some people will

admonish governments to stand up to markets. But when you are relying on

capital markets to finance a large part of your continuing budget deficit and

your debt rollover, this is empty bravado.

European governments should never have put their heads

so far into the lion’s mouth with regard to public sector borrowing. But

the politicians – and many others – convinced themselves that they were all

going to become more like Germany.

Peripheral Europe will never be like Germany.

It’s time to face the implications of that fact.

No comments:

Post a Comment