Money, Savings and Debt

by Pater Tenebrarum

This post

can in a way be seen as an addendum to what we wrote regarding the 'gold narrative' the other day. Specifically,

we want to return to the argument made in closing, namely that the present

situation in terms of private and public debt relative to the economy's ability

to create enough wealth to service and repay said debt is a reason to remain

bullish on gold and by extension, to remain skeptical regarding the economy's

future.

It is

important to keep in mind that the level of outstanding debt

as such actually does not prove the point. For instance, if all the credit

extended were backed by real savings and if the great bulk of

the extended credit were employed productively, then the size of the debt would

obviously not represent a problem. After all, we would then have very good

reason to expect that the investments that have been undertaken are largely

sound (given the fact that they are backed by real savings) and that therefore,

the economy's future output of final goods will increase sufficiently to create

the profits required to service and repay the debt.

However, we

know for a fact that a vast portion of the debtberg does not consist of credit

that has been productively employed. Moreover, we also know for a fact that

much of it is not backed up by real savings. How do we know all this?

Let us first

discuss savings. What are savings? In a monetary economy, people save in the

form of money. Money is a claim on real goods, it is the ultimate present good.

However, in order to save, one has to refrain from consumption. Let us say that

someone saves $200 per month. He certainly could spend these $200 instead of

saving them, in which case he would exert a claim on the pool of final goods

and consume the goods purchased. Note that by refraining from this act of

consumption, not only are there now $200 in his savings account, but the goods

the saver has not consumed remain with the economy's pool of real funding (the

pool of real funding is the stock of produced, but unconsumed final goods).

This

addition to the pool of real funding is what actually makes an increase in

production possible. If ten savers put aside $200 per month, the

$2,000 worth of goods thus saved could e.g. be used to maintain the life and

well-being of one worker employed in production activities. When an entrepreneur

applies to a bank for credit in order to expand production, he is ultimately

not trying to obtain money as such, but capital. What is required

to effectively fund new production activities is not money, but real resources.

To

illustrate this, imagine that a few people find themselves stranded on a

deserted island, and by coincidence one of the things that has been

successfully recovered from the shipwreck is a printing press for banknotes and

all the paraphernalia required for the printing process. Obviously they could

not create any wealth for themselves by printing banknotes. It would be a

pointless exercise: the banknotes could not be used to buy the necessary

capital goods required to e.g. build a new boat, since these goods are simply

not available on the island. This would be so glaringly obvious that they would

certainly not even try – they could print billions and would not be an iota

richer. If they decide to mix their labor with the natural resources available

on the island so as to create primitive capital goods that bring them a few

steps closer to their goal of building a boat, they would still be confronted

with the problem that at the outset, their pool of real funding would be zero.

They would at first have to produce whatever is necessary to keep them alive

(i.e., food). If they want to spend time on producing capital goods, enough

food would have to be produced that some of it could be saved to maintain their

lives while they are busy with building an ax, a net, rudders, sails and so

forth.

This example

serves to highlight a universal truth: no wealth can be created by

printing money. Money is indispensable for an economy based on the division of

labor, as a medium of exchange (and all the subsidiary functions that flow from

this, such as the store of wealth function) and a unit of account that enables

economic calculation. It should be obvious though that adding to the supply of

money does not add to the economy's wealth (in case a commodity money is used,

it could be argued that the non-monetary uses of the commodity make additional

supplies valuable beyond their exchange value, but as a rule the general medium

of exchange derives the great bulk of its value from monetary demand).

Since 1971,

the world has been on a fiat money standard. Moreover, the banking system is

fractionally reserved, which means that it can literally create additional

money from thin air. There is no effort involved except a few keystrokes. This

system is backstopped by central banks that 'accommodate' this creation of

money from thin air by supplying bank reserves, which are likewise created at

the push of a button. In this system, a lot of credit is created that is not

backed by real savings. We can get an inkling regarding the size of this credit

creation from thin air by looking at the amount of uncovered money substitutes

in the economy, i.e., deposit money that is not backed by standard money in the

form of currency or bank reserves which can be converted to currency on demand.

US money

TMS-2 by economic categorization. Covered money substitutes (dark blue) consist

of deposit money that is backed by either vault cash or bank reserves held at

the Fed. Uncovered money substitutes (also known as 'fiduciary media')

represent deposit money that has literally been created from thin air and for

which no standard money backing exists – click to enlarge.

As can be

seen above, although the Fed's 'quantitative easing' policy has vastly

increased the portion of money substitutes that are covered by bank reserves

(the often cited excess reserves), the amount of uncovered money substitutes

outstanding nevertheless stands at a new record high. In theory, all of this

money should be available on demand. In practice, the banks could only pay out

the covered portion and would have to contract credit if they were required to

pay out more than that.

The main

problem with the creation of money from thin air is that by throwing additional

fiduciary media on the loan market, the market interest rate is pushed below

the natural interest rate dictated by society-wide time preferences. This sets

the boom-bust cycle into motion. The lower interest rate makes long-term

investment projects that appeared to be unprofitable at a higher rate look

profitable, so investment will be drawn toward such projects. The lower market

interest rate suggests that the pool of real savings has increased so as to

make the funding of these long-range investment projects possible. However,

this is a mirage: the additional real savings do in fact not exist. To

paraphrase Mises, the entire class of entrepreneurs finds itself in a situation

akin to that of a master builder who attempts to build a palace with three

stories, while unbeknown to him, the building material available is only

sufficient for two stories. Obviously, the later he discovers this error, the

more significant the loss will be, as a lot of resources will have been wasted.

Moreover,

the creation of fiduciary media makes exchanges of nothing for

something possible. The early receivers of newly created money can

exercise claims on the pool of real savings, although no commensurate

contribution to the pool has actually been made. The earlier receivers of newly

created money will benefit to the detriment of later receivers, as by the time

the new money has percolated through the economy, prices will have risen to

reflect the increase of the money supply. Obviously, the earlier in the process

one gets to spend newly created money, the bigger one's advantage will be. Thus

wealth is redistributed from late to early receivers. Moreover, by exercising

their claim without an offsetting contribution to the pool of real savings

having been made, these early receivers make life more difficult for genuine

wealth creators, who now must contend with a diminished pool of savings. In

short, printing additional money enables consumption without preceding

production. Obviously this cannot possibly be sustainable – ultimately

consumption is constrained by production (one cannot consume what hasn't first

been produced).

In a

nutshell the problem posed by the mountain of debt that has been built up over

time is the following: it has misdirected investment and falsified economic

calculation, which in turn has distorted the structure of production and led to

the consumption of scarce capital (which is usually disguised as illusionary

accounting profits) during the boom periods. Subsequently this became painfully

obvious as the inevitable economic busts set in.

What's more,

the duration and amplitude of the boom-bust sequences has continually grown, as

after every failed boom, the amount of new credit and money thrown at the economy

to 'rescue' it from the bust has been vastly increased. Ever larger additions

to the amount of money and debt outstanding have resulted in ever smaller

additions to economic output.

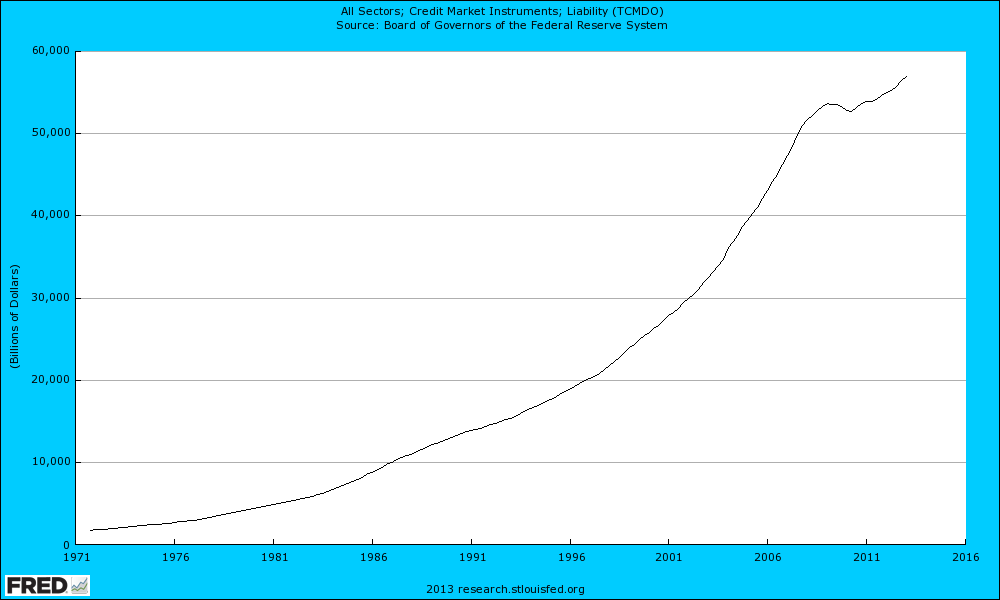

US: total credit market debt outstanding – click to enlarge.

If we

consider the total amount of credit market debt outstanding depicted above, it

is clear that large portions of this debt are indeed unproductive and represent

a millstone hanging around the economy's neck. There are for instance (in the

case of the US) more than $16 trillion in cumulative public debt. This

represents the government's debt-financed consumption of the past. Even those

who erroneously believe deficit spending to be economically beneficial must

realize that this debt that is the residual of past deficit spending can only

harm future economic development.

US: total public debt on the federal level – click to enlarge.

As Ludwig

von Mises wrote regarding this point in Human Action:

“But if the government invests

funds unsuccessfully and no surplus results, or if it spends the money for

current expenditure, the capital borrowed shrinks or disappears entirely, and

no source is opened from which interest and principal could be paid. Then

taxing the people is the only method available for complying with the articles

of the credit contract. In asking taxes for such payments the

government makes the citizens answerable for money squandered in the past. The

taxes paid are not compensated by any present service rendered by the

government's apparatus. The government pays interest on capital which has been

consumed and no longer exists. The treasury is burdened with the unfortunate

results of past policies.”

(emphasis

added)

We would

note to this: one of the many Achilles heels of deficit spending that aims to

provide 'economic stimulus' is precisely that the wealth creators in the

economy know very well that they will eventually be taxed to pay for it. It is

a good bet their reaction will reflect this knowledge. They will become

cautious, take fewer risks and curtail their investment activities. This is one

of the reasons why massive deficit spending schemes such as that enacted in

Japan over the past two decades consistently fail to work.

Another

point worth considering is that there is also still a vast amount of mortgage

debt outstanding that is effectively 'underwater'. The collateral is worth less

than the remaining debt, as a consequence of the housing bubble. No-one dares

to write this unsound debt off, as doing so would denude the banks of capital.

And so various extend and pretend schemes have been enacted (ranging from the

adoption of dubious accounting methods to delaying foreclosure proceedings to

various tax-payer funded interventionist schemes that aim to prevent a

write-off of this debt). This is in many ways a drag on the economy, as both

lenders and potential borrowers are paralyzed by this overhang of unsound debt.

Wealth Creation in the Market Economy and the State

In spite of

the foregoing, it is important to stress that the market economy, even though

it is extremely hampered, continues to create wealth. We once attended a

presentation by Professor Hans-Hermann Hoppe, in which he discussed the 2008

crisis and its aftermath. There was one remark he made during the Q&A that

struck us as especially pertinent to this discussion. He essentially said (we

are paraphrasing from memory): “We can gauge how powerful the market

economy's ability to create wealth is by considering that in most modern-day

regulatory democracies, perhaps 30% of the population can be said to be

involved in genuine wealth creation activities. In spite of the fact that the

entire amount of wealth is created by this small minority, and that this

minority is subjected to the most onerous regulations and taxes, it still

manages to improve the well-being and standard of living of all of society over

time.”

Along

similar lines, Mises stressed that although an artificial credit-induced boom

leads to impoverishment, this does not mean that we should expect that we will

necessarily be poorer overall at the end of a boom than at its beginning. This

is so because even under the unhealthy conditions of a boom, genuine wealth

creation continues. If that were not the case, the capitalist system wouldn't

have been able to increase the world's stock of wealth continually ever since

capitalist production processes have been adopted. However, it is also

important to realize that all of this has happened in spite of

the hampering of the market economy by taxation and regulations and the failed

central economic planning by central banks.

Obviously

though, there must be a limit to the depredations the economy can handle.

Today, the State has created an environment in which most of the intellectuals

who propagate political and economic ideas are essentially bought off, as the

government can offer them levels of remuneration that are way beyond the value

their services would command in a free market. Naturally they will tend to sotto

voce engage in the vilest statist propaganda. Very few dare to bite

the hand that feeds them, even if they are aware that they are promoting a

harmful ideology. Presumably, quite a few of them even believe in what they are

promoting.

We can see

this in many obvious contradictions, such as the fact that e.g. most economists

today agree that the market economy represents the by far best system for

creating wealth, but at the same time support fiat money and central economic

planning by the central bank, deficit spending by the state, and all sorts of

state interventions in the economy. This is an inconsistent position. Either

the free market is the best system, or its opposite, full-blown socialism, is.

It is simply absurd to claim that what we really need is just enough socialism

so as not to kill off the market economy altogether.

We are happy

to report though that the intellectual handmaidens of statism are finding it

ever more difficult to propagate their memes due to the internet having opened

up alternative channels of communication and information that are outside of

establishment control. This has made it possible for many people to learn of

ideas that have previously been suppressed. On the other hand it is clear that

we are still very far from the tide having decisively turned.

In fact,

because the State now finds itself under increasing financial and economic

pressure, it reacts in a manner that it regards as the politically palatable

'solution' to the debt problem. This solution consists primarily of

inflationary policy (see the chart of TMS-2 above for evidence), and various

forms of 'financial repression'. Inflation mainly robs the poorest members of

society, while financial repression, depending on what forms it takes, robs

everyone. The alternatives, such as writing off the unsound debt that has

accumulated or cutting unsustainable government spending, are policies that are

regarded as highly detrimental to winning elections. The welfare state has

created so many dependents and hangers-on, not least including a vast and powerful

class of bureaucrats who represent a large block of votes, that no politician

dares to veer off established lines too much. Hence financial repression is

chosen as the 'lesser evil' from the point of view of the ruling classes (whose

main aim it is to preserve their rule and privileges).

However,

there is a big problem with this. As the above-mentioned Professor Hoppe e.g.

remarks in “The Economics and Ethics of Private Property” with regard to

taxation:

“Thus, by coercively

transferring valuable, not yet consumed assets from their producers (in the

wider sense of the term including appropriators and contractors) to people who

have not produced them, taxation reduces producers’ present income and their

presently possible level of consumption. Moreover, it reduces the present

incentive for future production of valuable assets and thereby also lowers

future income and the future level of available consumption. Taxation is not

just a punishment of consumption without any effect on productive efforts; it is

also an assault on production as the only means of providing for and possibly

increasing future income and consumption expenditure. By lowering the present value associated

with future-directed,

value-productive efforts, taxation raises the effective rate of time

preference, i.e., the rate of originary interest and, accordingly, leads to a

shortening of the period of production and provision and so exerts an

inexorable influence of pushing mankind into the direction of an existence of

living from hand to mouth. Just increase taxation enough, and you will have

mankind reduced to the level of barbaric animal beasts.”

Hoppe also

points out that regulations (which compel or prohibit exchanges between private

parties), while they are just as economically harmful as taxation, don't

increase the economic resources in the hands of the government. They merely

satisfy the lust for power. He concludes that this is the main reason why in

wars between industrialized Western States, the less regulated ones tended to

win against the more regimented ones.

However, we

would point out that even the US economy, which is still widely regarded as one

of the less hampered and regulated Western economies, boasts the following

statistics as of 2012 (Source: the Ten Thousand Commandments):

• Total costs for

Americans to comply with federal regulations reached $1.806 trillion in 2012.

For the first time, this amounts to more than half of total federal spending.

It is more than the GDPs of Canada or Mexico.

• This is the 20th anniversary

of Ten Thousand Commandments. In the 20 years of publication, 81,883

final rules have been issued. That’s more than 3,500 per year or about nine per

day.

• The Anti-Democracy Index –

the ratio of regulations issued to laws passed by Congress and signed by the president

– stood at 29 for 2012. That’s 127 new laws and 3,708 new rules – or

a new rule every 2 ½ hours.

• Regulatory costs

amount to $14,678 per family – 23 percent of the average household income of

$63,685 and 30 percent of the expenditure budget of $49,705 and more than

receipts from corporate and personal income taxes combined.

• Combined with $3.53 trillion

in federal spending, Washington’s share of the economy now reaches 34.4

percent.

(emphasis added)

Read the rest at: