The foundation of lending is real wealth and not money as such

by Frank Shostak

Bruce Bartlett recently lamented in The

New York Times that given the current state of economic affairs we

need more Keynesian medicine to fix the US economy. According to Bartlett, the

core insight of Keynesian economics is that there are very special economic

circumstances in which the general rules of economics don’t apply and are in

fact counterproductive. This happens when interest rates and inflation rates

are so low that monetary policy becomes impotent; an increase in the money

supply has no boosting effect because it does not lead to additional spending

by consumers or businesses. Keynes called this situation a “liquidity trap.”

Keynes wrote,

There is the possibility ... that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest.[1]

Bartlett holds that:

Under such circumstances government spending can be highly stimulative, because it causes money that is sitting idle in bank reserves or savings accounts to circulate and become mobilized through consumption or investment. Thus monetary policy becomes effective once again.

Bartlett regards this as an extremely

important insight that policy makers have yet to grasp. According to our

columnist, despite massive monetary pumping by the Fed since 2008, it has

produced very little boosting effect on the economy. The Fed’s balance sheet

jumped from $0.897 trillion in January 2008 to $3.3 trillion

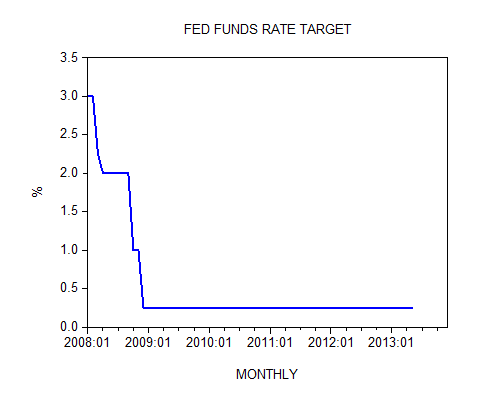

in early May 2013. The Federal Funds Rate target stood at 0.25 percent

in early May against 3 percent in January 2008.

According to Bartlett,

In normal times, one would expect such an increase in the money supply to be highly inflationary and sharply raise market interest rates. That this has not happened is proof that we have been in a liquidity trap for several years. We needed a lot more government spending than we got to get the economy out of its doldrums.

Note also that Nobel Laureate in economics

Paul Krugman holds similar views. For them what is needed is a re-activation of

the monetary flow that somehow got stockpiled in the banking system. Observe

that in the Keynesian framework the ever-expanding monetary flow is the key to

economic prosperity. What drives economic growth is monetary expenditure.

Why is money not the driver of economic

growth?

Contrary to popular thinking, monetary

flow has nothing to do with economic growth as such. Money is simply a medium

of exchange and nothing more than that. Also, note that people don’t ultimately

pay for goods and services with money, but rather with the goods and services

that they have produced.

For instance, a baker pays for shoes by

means of the bread he produced, while the shoemaker pays for the bread by means

of the shoes he made. When the baker exchanges his money for shoes, he has

already paid for the shoes, so to speak, with the bread that he produced prior

to this exchange.

Again, money is just employed to exchange

goods and services. Being the medium of exchange, money can only assist in

exchanging the goods of one producer for the goods of another producer.

What drives economic growth is savings

that are used to fund the increase and the enhancement of tools and machinery,

i.e., capital goods or the infrastructure that permits the increase in final

goods and services: real wealth to support the lives and well being of people.

Contrary to popular thinking, an increase

in the monetary flow is in fact detrimental to economic growth since it sets in

motion an exchange of something for nothing — it leads to the diversion of real

wealth from wealth generators to wealth consumers. This in the process reduces

the amount of wealth at the disposal of wealth generators thereby diminishing

their ability to enhance and maintain the infrastructure. This in turn

undermines the ability to grow the economy.

What is behind the so called liquidity

trap?

The fact that so far the Fed’s massive

pumping has not resulted in a massive monetary flood should be regarded as good

news. If all that new money were to enter the economy, it would have entirely

decimated the machinery of wealth generation and produced massive economic

impoverishment.

It seems that market forces have so far

managed to withstand the onslaught by the US central bank. What allowed this

resistance is not some kind of ideology against aggressive pumping by the Fed

(in fact most experts and commentators are of the view that the Fed should

create a lot of money in difficult times), but the fact that the process of

real wealth generation has been severely damaged by the previous loose monetary

policies of Greenspan’s and Bernanke’s Fed.

The badly damaged process of wealth

generation has severely impaired true economic growth, and obviously this has

severely reduced good quality borrowers and subsequently has reduced banks

willingness to lend. Remember that in essence banks actually lend real wealth

by means of money. They are just intermediaries. Obviously then, if wealth

formation is being impaired, less lending can be done. We suggest that it is

this fact alone that explains why all the pumping by the Fed has ended up

stacked in the banking system. So far in early May banks have been sitting on

over $1.7 trillion in surplus cash. In January 2008 surplus cash stood at $2.4 billion.

Given the high likelihood that the process

of real wealth generation has been severely damaged, this means that the pace

of wealth generation must follow suit. Now, contrary to popular thinking an

increase in government spending cannot revive the process of wealth generation,

but on the contrary it can only make things much worse.

Remember government is not a

wealth-generating entity, so in this sense increases in government spending

generate the same damaging effect as monetary printing does; it leads to the

diversion of wealth from wealth generators to wealth consumers. Observe that in

2012, US government outlays stood at $3.538 trillion, an increase

of 98 percent from 2000.

As long as the rate of growth of the pool

of real wealth stays positive, this can continue to sustain productive and

nonproductive activities.

Trouble erupts, however, when, on account

of loose monetary and fiscal policies, a structure of production emerges that

ties up much more wealth than the amount it releases.

This excessive consumption relative to the

production of wealth leads to a decline in the pool of wealth.

This in turn weakens the support for

economic activities, resulting in the economy plunging into a slump. The

shrinking pool of real wealth exposes the commonly accepted fallacy that loose

monetary and fiscal policies can grow the economy.

Needless to say, once the economy falls

into a recession because of a shrinking pool of real wealth, any government or

central-bank attempts to revive the economy must fail.

This means that a policy such as lifting

government outlays to counter the liquidity trap will make things much worse.

Not only will these attempts not revive

the economy; they will deplete the pool of real wealth further, thereby

prolonging the economic slump.

Likewise any policy that forces banks to

expand lending “out of thin air” will further damage the pool and will further

reduce banks’ ability to lend.

Again the foundation of lending is real

wealth and not money as such. It is real wealth that imposes restrictions on

banks’ ability to lend. (Money is just the medium of exchange, which

facilitates the flow of real wealth.)

Note that without an expanding pool of

real wealth, any expansion of bank lending is going to lift banks’

nonperforming assets.

Summary and conclusion

Contrary to various experts, we suggest

that in the current economic climate an increase in government outlays is not

going to make Fed’s loose monetary policies more effective as far as boosting

economic activity is concerned.

On the contrary, it will weaken the

process of wealth generation and will retard economic growth.

What is needed to get the economy going is

to close all loopholes for money creation and drastically curtail government

outlays.

This will leave a greater amount of wealth

in the hands of wealth generators and will boost their ability to grow the

economy.

(1) John Maynard Keynes, The General Theory of Employment, Interest, and Money, MacMillan &

Co. Ltd. (1964), p. 207.

No comments:

Post a Comment