A Question of

Spending Discipline and Reform

by Pater

Tenebrarum

The Baltic States

are unique in Europe in that they went through an austerity crash program a

while ago already (beginning right after the 2008 crisis) and have in the

meantime recovered strongly. Der Spiegel has an interesting interview with

Lithuanian president Dalia Grybauskaite, in which she explains her views on the

topic. It can obviously be done successfully.

Just to get this

out of the way up front: we are aware that every case is unique. The problems

are not the same in every country, and due to cultural norms and traditions, it

may be easier to enact reform in certain countries than others. Nevertheless,

no matter how many times Paul Krugman insists that no Baltic nation can

possibly be held up as an example, the fact remains that they have imposed

fiscal austerity and implemented wide-ranging reform measures and have

succeeded.

Here are a few

notable excerpts from the interview:

“SPIEGEL ONLINE: In spite of the ongoing crisis, Lithuania wants to join the euro zone in January 2015. Why?

Grybauskaite:This is not a crisis of the euro zone, but a debt crisis. Some states, inside and outside the euro zone, have difficulties because of their irresponsible economic and fiscal policies. […]

SPIEGEL ONLINE: A new poll in six big EU countries shows that trust in the EU is declining rapidly. Are EU leaders taking this growing unease seriously enough?

Grybauskaite:This is the consequence of the crisis in Europe and people's reaction to the inability of the politicians to tackle the challenges.

SPIEGEL ONLINE: The president of the EU commission, José Manuel Barroso, said this week that austerity in Europe had reached its limit. The political and social acceptance is not there any longer. Is it time to relax the efforts?

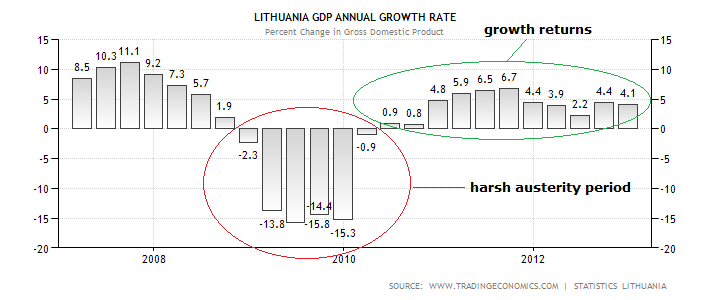

Grybauskaite: There is not one rule you can apply to every state. In the Baltic states, after 2009 we had to implement very radical austerity measures. In Lithuania, we consolidated 12 percent of GDP in two years. We cut public salaries by 20 percent and pensions by 10 percent. Our adjustment was a lot deeper than what we see now in Southern Europe. And we saw growth return after 2 years.

SPIEGEL ONLINE: So Barroso is wrong?

Grybauskaite: Some countries need extra stimulus in specific areas. Something has to be done against high youth unemployment in Greece and Spain, for example. But in the end, there is no way around it: The debt levels have to come down.

SPIEGEL ONLINE: You say that reducing public debt is mainly about political will. Where do you see this will lacking in Europe?

Grybauskaite: I won't name countries, but reforms could be quicker in many parts. There are different mentalities and different ideas about political responsibility in the North and the South.

SPIEGEL ONLINE: Austerity is often seen as a diktat from Germany. From the perspective of a small country, is Berlin too powerful?

Grybauskaite: We need to understand the situation of the German people. They are largely responsible for paying for these bailouts. I cannot imagine a head of government whose country is paying for something not asking for certain conditions. It is legitimate that Berlin leads the way.” (emphasis added)

Takeaways:

She is right – as

we have often pointed out in these pages, it is not a currency crisis,

but a debt crisis. The euro as such seems to be doing fine, as well as

can be expected from a modern fiat currency. It is the private and public

sector debt mountains that have been built up over time that are the problem,

not the fact that several nations use a common currency.

One might of

course counter 'the common currency has caused debts to increase so much', but

that is only partially true. We cannot recall that Italy or Greece had any

problems growing their debt into the blue yonder in the past, i.e.,prior

to the adoption of the euro. The main difference is that they used to be able

to devalue their way out of problems, thereby robbing their citizens

surreptitiously. At least nowadays the cost is quite obvious to all.

Take note of the

example she gives for austerity a la Lithuania (similar courses were followed

in the other Baltic nations):

“We cut public salaries by 20 percent and pensions by 10 percent. Our adjustment was a lot deeper than what we see now in Southern Europe. And we saw growth return after 2 years.”

The magic words

here are: “cut spending”. As opposed to “raise taxes, and then raise them some

more, while leaving spending almost exactly as it was before” – the preferred

method in places like Italy, Spain and Greece. Yes, the debt levels have to

come down – but it is not immaterial how they are coming down.

No doubt it was not exactly great fun to be in the Baltics during the harsh

period of adjustment. However, we are sure Greece's citizens would have been

more or less perfectly fine with just two years of hardship. It is vastly

different when the hardship is going into its fifth year with still no light at

the end of the tunnel. In this context, Mr. Barroso's recent proclamations

strike us as rather dubious. He seems to think there is a 'choice', but there

very likely isn't one, as markets will sooner or later penalize countries

veering from their fiscal consolidation efforts.

Cutting spending

is not everything of course – economic reform is just as, if not more

important. This is another area where many European governments are lacking the

necessary political will and imagination. The Baltic nations still have

memories of Soviet Russia's embrace – that does wonders for one's political

will and the ability to endure hard times for a little while.

And finally,

yes, the paymasters must be expected to insist on conditions for keeping

others afloat. Imagine if things were the other way around: if Italy, Spain,

Greece, etc., were asked to bail out Germany and Finland, would they be doing

so without demanding conditions? Not

very likely, is it?

Lithuania: a

bubble, followed by a severe bust coupled with austerity, and the return of

growth- click to enlarge.

The ups and downs of industrial production in Lithuania. Note that production

began to improve well before the contraction in GDP ended- click to enlarge.

The budget deficit as a percentage of GDP. Lithuania is already getting close

to the Maastricht ratio again – click to enlarge.

Conclusion:

There are ways and

means to deal with a major bust and fiscal troubles. None of them are painless,

but some make more sense than others.

No comments:

Post a Comment