At the present

slow pace of job growth, it will require more than a decade to get back to full

employment defined by pre-recession standards

The market tanked Wednesday on bad preliminary job news. And so, when

Friday's jobs report is released, the unemployment rate and the number of new

jobs will come in for close scrutiny. Then again, they always attract the most

attention. Even the Federal Reserve focuses on the unemployment rate,

announcing on a number of occasions that a rate of 6.5% will indicate when it

is time to start raising interest rates and winding down the Fed's easy-money

policies.

Yet the unemployment rate is not the best guide to the strength of the

labor market, particularly during this recession and recovery. Instead, the Fed

and the rest of us should be watching the employment rate. There

are two reasons.

First, the better measure of a strong labor market is the proportion of the

population that is working, not the proportion that isn't. In 2006, 63.4% of

the working-age population was employed. That percentage declined to a low of

58.2% in July 2011 and now stands at 58.6%. By this measure, the labor market's

health has barely changed over the past three years.

Second, the headline unemployment rate, what the Bureau of Labor Statistics

calls "U3," uses as its numerator the number of individuals who are

actively seeking work but do not have jobs. There is another highly relevant

measure that captures what is going on in the economy. "U6" counts

those marginally attached to the workforce—including the unemployed who dropped

out of the labor market and are not actively seeking work because they are

discouraged, as well as those working part time because they cannot find

full-time work.

Second, the headline unemployment rate, what the Bureau of Labor Statistics

calls "U3," uses as its numerator the number of individuals who are

actively seeking work but do not have jobs. There is another highly relevant

measure that captures what is going on in the economy. "U6" counts

those marginally attached to the workforce—including the unemployed who dropped

out of the labor market and are not actively seeking work because they are

discouraged, as well as those working part time because they cannot find

full-time work.

Every time the unemployment rate changes, analysts and reporters try to

determine whether unemployment changed because more people were actually

working or because people simply dropped out of the labor market entirely,

reducing the number actively seeking work. The employment rate—that is, the

employment-to-population ratio—eliminates this issue by going straight to the

bottom line, measuring the proportion of potential workers who are actually

working.

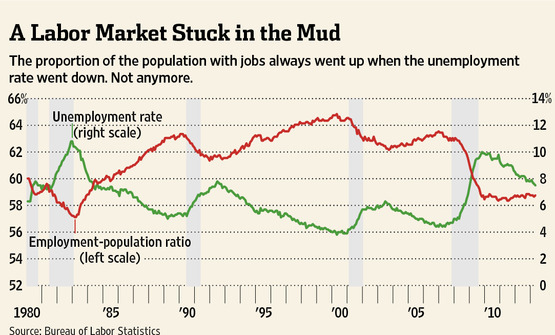

During the past three decades the relation between unemployment and

employment has been almost perfectly inverse. (See the nearby chart.) When the

employment-to-population ratio rises, the unemployment rate falls. When the

unemployment rate rises, the employment-to-population ratio falls. Even the

turning points are aligned. Consequently, the unemployment rate has been a very

good proxy for the employment rate. But that relationship has completely broken

down during the most recent recession.

While the unemployment rate has fallen over the past 3½ years, the

employment-to-population ratio has stayed almost constant at about 58.5%, well

below the prerecession peak. Jobs are always being created and destroyed, and

the net number of jobs over the last 3½ years has increased. But so too has the

size of the working-age population. Job growth has been just slightly better

than what it takes to keep the employed proportion of the working-age

population constant. That's why jobs

still seem so scarce.

The U.S. is not getting back many of the jobs that were lost during the

recession. At the present slow pace of job growth, it will require more than a

decade to get back to full employment defined by prerecession standards.

The striking deficiency in jobs is borne out by the Bureau of Labor

Statistics' Job Openings and Labor Turnover Survey. Despite declining

unemployment rates, the number of hires during the most recent month (March

2013) is almost the same as it was in January 2009, the worst month for job

losses during the entire recession (4.2 million then, 4.3 million now).

Why have so many workers dropped out of the labor force and stopped

actively seeking work? Partly this is due to sluggish economic growth. But

research by the University of Chicago's Casey Mulligan has suggested that

because government benefits are lost when income rises, some people forgo poor

jobs in lieu of government benefits—unemployment insurance, food stamps and

disability benefits among the most obvious. The disability rolls have grown by

13% and the number receiving food stamps by 39% since 2009.

These disincentives to seek work may also help explain the unusually high

proportion of the unemployed who have been out of work for more than 26 weeks.

The proportion of unemployed who are long-termers reached 45% in April 2010 and

again in March 2011. It is still above 37%. During the early 1980s, when the

economy experienced a comparable recession, the proportion of long-term

unemployed never exceeded 27%.

The Fed may draw two inferences from the experience of the past few years. The

first is that it may be a very long time before the labor market strengthens

enough to declare that the slump is over. The lackluster job creation and

hiring that is reflected in the low employment-to-population ratio has

persisted for three years and shows no clear signs of improving.

The second is that the various programs of quantitative easing (and other

fiscal and monetary policies) have not been particularly effective at

stimulating job growth. Consequently, the Fed may want to reconsider its decision

to maintain a loose-money policy until the unemployment rate dips to 6.5%.

No comments:

Post a Comment